The 6% Mandate: Why 94% of AI Investments Aren't Moving the Needle on Profit

The Capital Mirage: Why AI Ubiquity Fails to Generate Alpha

The saturation of AI across the global enterprise landscape has reached a point of profound fiscal decoupling. While data from McKinsey & Company indicates that 90% of organizations have integrated AI into at least one functional vertical, this deployment is largely an exercise in technical theater rather than value creation [1].

The current surge in capital expenditure has fostered an adoption bubble where the appearance of digital maturity masks a systemic failure to drive bottom-line growth. The data confirms a stark divide: a mere 6% of enterprises attribute more than 5% of their earnings before interest and taxes (EBIT) to AI-driven initiatives [1].

For the remaining 94%, the investment remains a speculative cost center, failing to move the needle on corporate profitability.

The Architecture of Failure

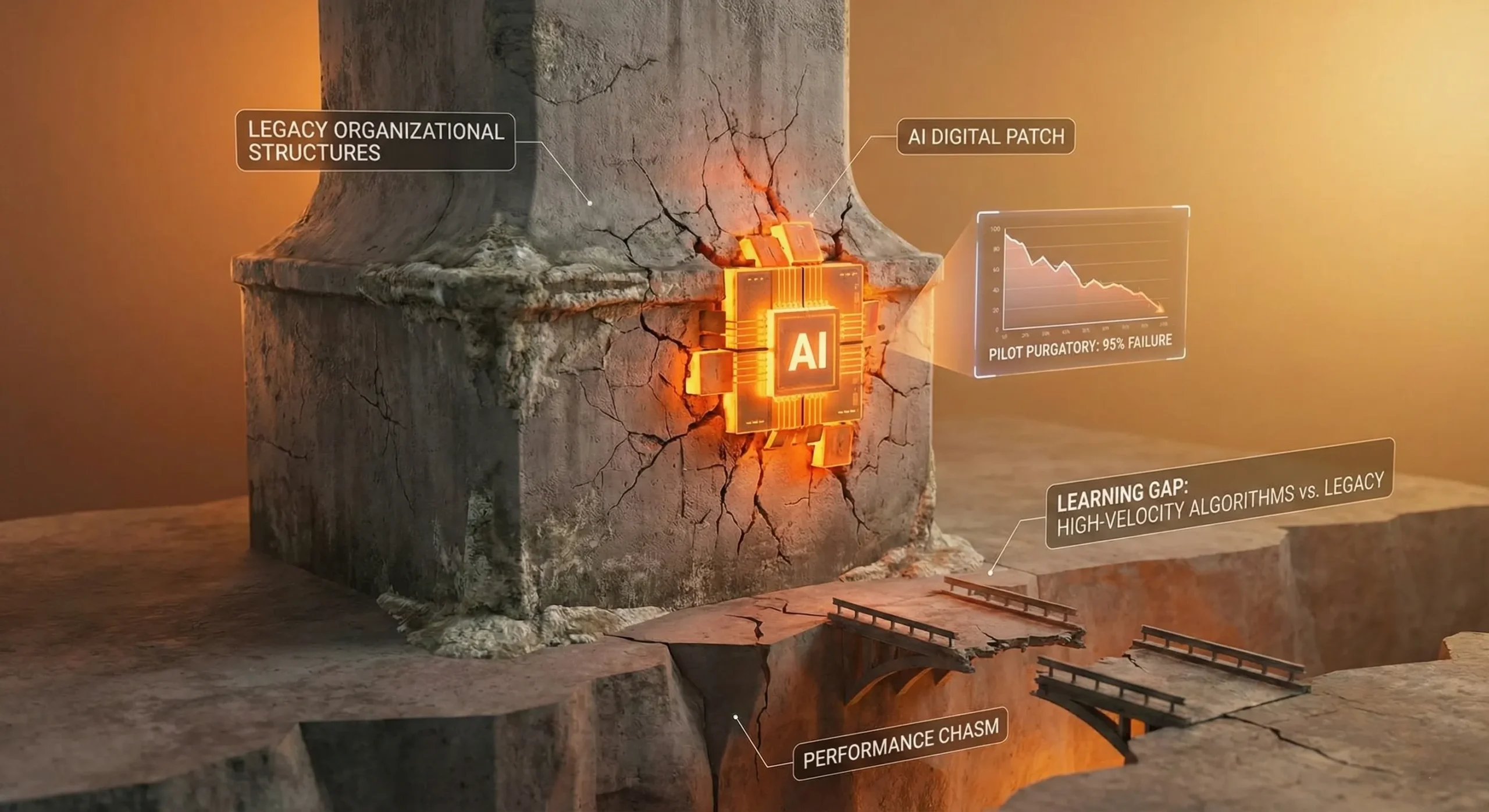

This performance chasm is not a product of technological scarcity but an expression of architectural liability. The vast majority of firms treat AI as a "digital patch"—a modular tool intended to accelerate existing, calcified workflows. This strategy is fundamentally flawed; it serves only to automate inherent inefficiencies.

The crisis is most visible in what MIT researchers identify as "pilot purgatory," where 95% of generative AI initiatives fail to achieve a measurable impact on the profit and loss statement [2]. Generic models, while flexible, remain isolated from the specific operational logic of the firm, creating a "learning gap" that prevents institutional integration.

The Strategic Imperative

For leadership, the era of incrementalism must end. The "tooling" mindset—purchasing software to solve isolated problems—has created "islands of automation" that leave the core operational DNA of the organization untouched.

Success demands institutional readiness: a total alignment of data infrastructure with strategic goals. Until the firm is rebuilt to treat data as a primary asset rather than a secondary output, AI will remain a fiduciary risk rather than a defensible competitive moat.

The 6% Playbook: A Blueprint for Real Value

So, what sets the high-performing 6% apart? The divide between the 6% of enterprises extracting significant EBIT from artificial intelligence and the 94% stagnating in pilot purgatory is not a product of luck, but of rigorous structural discipline. High performers are three times more likely to have fundamentally redesigned their workflows to be AI-native rather than merely augmenting legacy processes [1].

| Operational Dimension | Standard Firm (The 94%) | High Performer (The 6%) |

|---|---|---|

| Integration Strategy | Digital Patching: AI is a modular "bolt-on" to existing, calcified systems, automating technical debt. | Structural Logic: Workflows are fundamentally redesigned to be AI-native. |

| Example: Compliance | Reactive: AI expedites data extraction from single documents. | Proactive: AI ingests, classifies, and flags anomalies in real-time across the enterprise. |

| Leadership | Siloed: AI relegated to IT departments; treated as a cost-saving exercise. | Ownership: C-suite leaders demonstrate direct ownership; treated as a core business driver. |

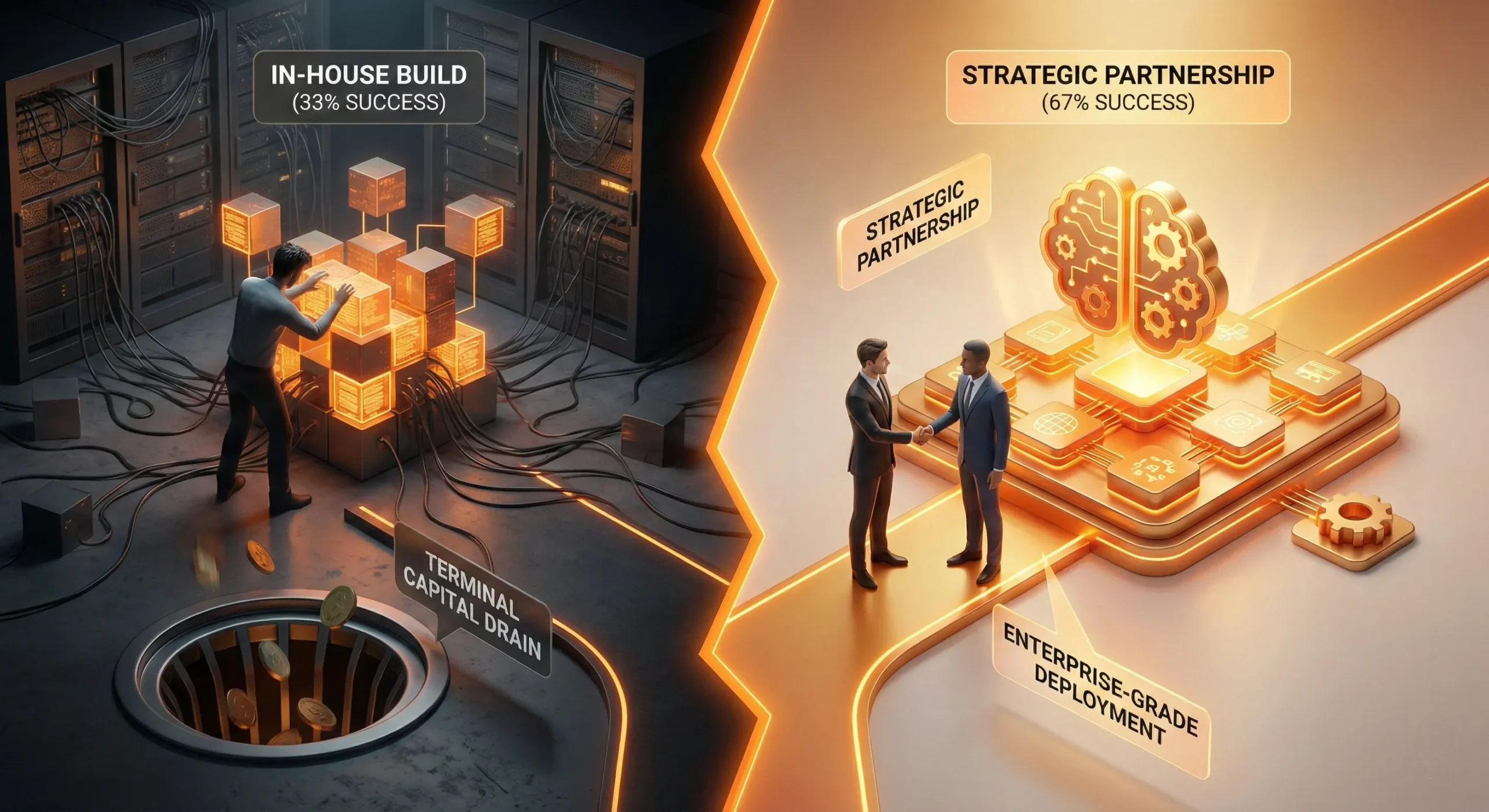

The Build-Buy Fallacy

The strategic allocation of capital is further complicated by the decision to build proprietary systems in-house. MIT's data indicates a staggering disparity in success rates between internal builds and strategic partnerships [2].

For many firms, the drive to build proprietary generative AI systems in 2026 is becoming a terminal drain on capital.

Success hinges on selecting tools that integrate deeply with refined workflows and choosing partners who can navigate enterprise deployment.

The Mandate for Modern Leadership

Joining the ranks of the high performers requires a conscious strategic shift. It begins with asking the hard questions: Where are our most critical, high-friction workflows? Are we organized to tackle end-to-end process transformation? Is our leadership team truly aligned and committed to driving this change? Are we allocating resources to the areas where AI can deliver the most value?

At Studio AM, we partner with organizations to navigate this exact journey. We believe that technology is only as powerful as the strategy that guides it. Our focus is on helping you re-architect the core processes that drive your business, ensuring that your AI investment translates not just into isolated efficiencies, but into a measurable and material impact on your bottom line. The path to becoming an AI-powered enterprise is not about buying more technology; it's about building a smarter, more integrated way of working.

For the leaders willing to embrace this mandate, the rewards are waiting.

Connect us nowReferences

[1] McKinsey & Company. "The State of AI in 2025: Agents, Innovation, and Transformation." Global Survey, November 5, 2025. https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai

[2] Sheryl Estrada. "MIT report: 95% of generative AI pilots at companies are failing." Fortune, August 18, 2025. https://fortune.com/2025/08/18/mit-report-95-percent-generative-ai-pilots-at-companies-failing-cfo/

[3] Gartner, Inc. "Gartner Predicts Over 40% of Agentic AI Projects Will Be Canceled by End of 2027." Press Release, June 25, 2025. https://www.gartner.com/en/newsroom/press-releases/2025-06-25-gartner-predicts-over-40-percent-of-agentic-ai-projects-will-be-canceled-by-end-of-2027